THE 5G BUSINESS CASE THAT WORKS

Iain Gillott

Founder, President of iGR

5G is now being deployed by select mobile operators around the world, but there is a problem: the initial cost to build a 5G network far exceeds the expected initial revenues, such that payback on the network build is not expected until 2022 at the earliest and 2023 or later (depending on the global region) for any significant revenues.

So, the question is how can the mobile operators minimize the risk of building 5G networks, especially in the early years, while also providing value to consumers?

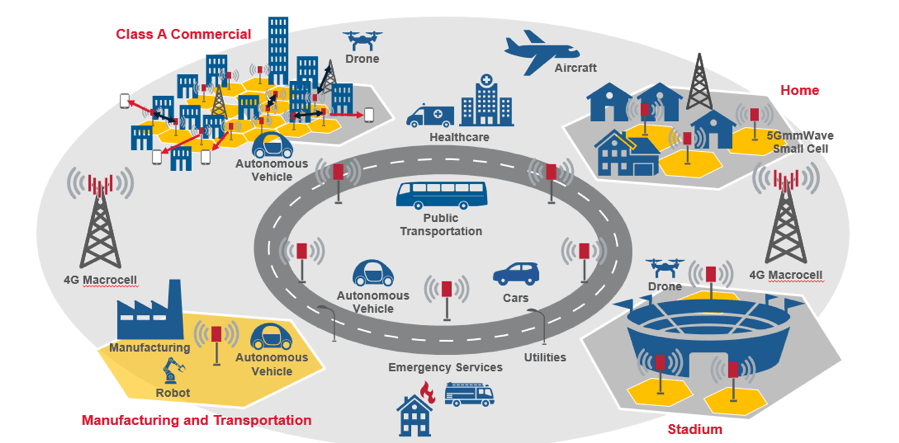

One way to shorten the payback period is to initially only build 5G ‘hotspots’ where the mobile operators need low latency to provide value-added services. Shown in the figure below – operators can start with building 5G hotspots (shown in yellow) to meet specific needs, applications, customers, etc., and maximize the current investment in LTE (shown in gray) to provide wide-area high bandwidth coverage. This architecture is the first step leading to full 5G deployment if needed.

4G and 5G network architecture – the interim step with 5G Hotspots

5G HOTSPOTS

The concept of an initial 5G build is to raise ‘hotspots’ of 5G where needed, for example in industrial sites, residential areas, malls, etc., essentially, areas of high traffic and/or high value for 5G. The operator would then need to promote 5G in those areas and maximize the benefit from the 5G applications and services to establish a proven revenue stream.

The macro network can then be upgraded to 5G as maintenance/updates dictate and to meet the increasing demand for 5G data capacity in that market. The impact of this approach is a faster return on the initial 5G build investment, which then provides supporting data for the continued 5G build as well as improved financials.

CAN EDGE COMPUTE BE LEVERAGED FOR 5G NEW CORE?

Part of the 5G build investment is obviously in the new 5G core, replacing the existing LTE EPC. While deploying 5G, mobile operators are also investing in edge computing to reduce latency. These investments are already in progress, providing hardware and software to support various apps and services.

Can this edge computing investment be leveraged to support the 5G ‘hotspots’? The edge computing architecture uses a distributed, virtualized environment that is deployed on off-the-shelf hardware. This is the same architecture that the 5G new core will use and realize an opportunity to co-locate the solutions and reduce deployment costs.

Consider that, according to iGR’s forecasts, the mobile operators globally will have to spend $25.6B on 5G new core between 2018 – 2023 if building out network-wide 5G. This spending is split among the various regions of the world according to 5G investment, with Asia Pacific responsible for the largest 5G new core spending.

However, the spending to put edge computing in the mobile network during this time is far less, at $387 million globally. Thus, if the edge computing architecture can be leveraged to support 5G, the potential savings are significant.

This real 5G business case cuts initial 5G investment and improves operator economics leveraging virtualization and edge computing to offer 5G services only where needed to increase revenue streams.